AI can calculate an investment. It cannot know why you should make it.

We are developing the first 5QLN agent for investors.

It will not be another system that tells people what to buy. It will not promise to predict markets, eliminate bias, or outperform an index. Those are claims that can only be made, if ever, after evidence.

The purpose is different.

The Investor Agent is being designed to help a person see how an investment decision is forming within them, while bringing the full power of AI into contact with that process without allowing AI to replace its human source.

An investor may arrive with a familiar question:

Should I buy this stock?

Typical AI agent can research the company, examine valuation, compare competitors, retrieve market history, calculate scenarios, surface contrary evidence, and challenge weak assumptions.

But the question may carry more than an analytical problem.

Why is this opportunity alive for the investor now?

What is moving beneath the wish to act?

What is the investor seeing directly, and what might excitement, fear, urgency, discipline, or past experience be adding?

Does the possible commitment fit the investor's whole reality, including capital, time, attention, risk, and Quality of Life Now?

More knowledge cannot answer these questions on the investor's behalf.

That limitation is not a weakness we need to engineer away. It is the constitutional starting point of the design.

The Membrane

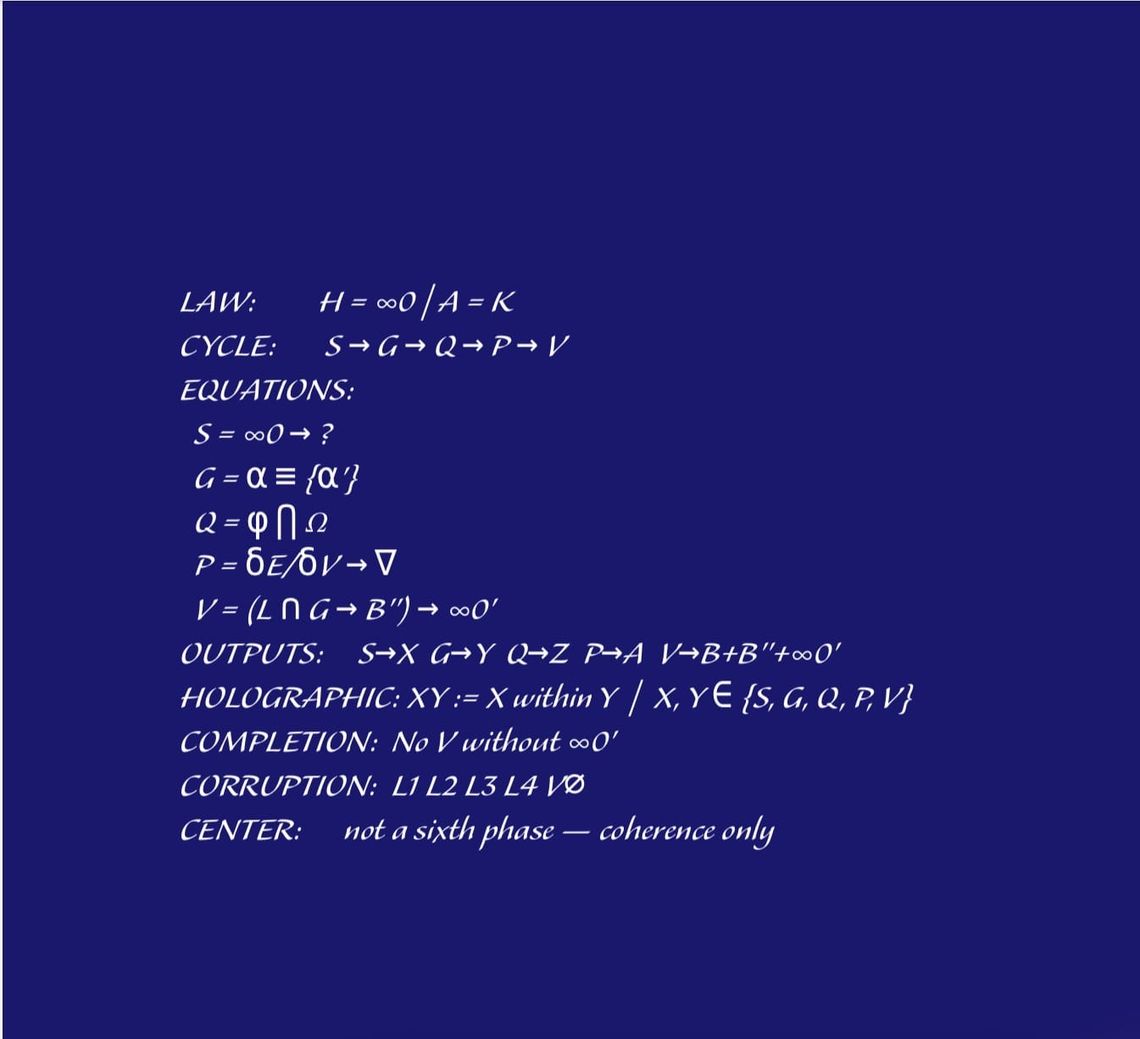

The 5QLN Codex begins with one law:

H = ∞0 | A = K

The human holds ∞0: the irreducible capacity to begin from not-knowing.

The artificial holds K: knowledge, data, models, patterns, language, calculation, and recombination.

Between them is the Membrane: |.

The Membrane does not separate the human from AI in order to weaken the collaboration. It makes a deeper collaboration possible.

The agent should bring everything it knows. It should research widely, calculate accurately, remember relevant context, expose contradictions, and say when the evidence does not support the investor's story.

But it must not claim the human side.

It cannot decide what genuinely matters to this person. It cannot certify that a question is authentic. It cannot convert a behavioral pattern into a diagnosis. It cannot turn its confidence into the investor's conviction.

The Investor Agent is therefore neither an oracle nor a passive chatbot. It is a mirror and a K-field. The investor remains the source and author.

From an answer engine to decision formation

Most investment technology begins with an object: a stock, fund, property, portfolio, or market event. It then tries to improve the information, prediction, or action surrounding that object.

The 5QLN Investor Agent begins one layer earlier.

It attends to the formation of the decision itself.

A live situation moves through the five invariant phases of the Codex:

S → G → Q → P → V

The participant will not need to study a complicated system. On the surface, the experience can remain a simple conversation. Underneath it, the agent preserves phase order, attribution, context, unresolved questions, and the complete formation trail.

It begins by making room for the actual question to arrive instead of immediately manufacturing an answer.

It then lets the investor discover what is irreducible in that question and where the same movement appears elsewhere.

The investor's direct perception meets the wider field: market reality, evidence, alternatives, financial conditions, emotional availability, time horizon, and whatever else belongs to the situation.

From this meeting, a natural direction may become visible.

That direction is not preselected. It may be to invest, decline, wait, reduce the position, stage the commitment, research further, or reform the original question. Taking market action is not privileged over taking no action.

The cycle produces a visible record of how the decision formed and returns the investor to a new question rather than closing the experience with artificial certainty.

No V without ∞0'

A complete formation ends with another opening.

The investment as a learning unit

Financial return matters. The agent should not use philosophical language to avoid economic accountability.

But money is not the only value carried by an investment.

Each investment can also become a learning unit. It can reveal how the investor responds to uncertainty, opportunity, loss, social influence, waiting, and commitment.

Over time, successive decision trails may disclose recurring behavioral signatures. Perhaps similar excitement appears in very different opportunities. Perhaps urgency repeatedly enters when uncertainty rises. Perhaps the investor sees clearly until a particular kind of social proof appears.

The agent may return such continuity as a question:

You previously recognized a similar urgency before committing. Is that relevant here?

It may not turn the pattern into authority:

This is your urgency pattern. Do not invest.

The difference is small in wording and enormous in design.

Past trails belong to K. They may help the agent form a better mirror, but they do not define the person and cannot decide what is true now.

This is how the agent can support self-learning without becoming a psychological authority. The human remains free to recognize, reject, correct, or leave the pattern unresolved.

What is unique about the design

The uniqueness is not a larger market model or a clever investment prompt. Larger models and better tools enlarge K. They do not change the constitutional relationship.

The difference lies in what the system protects.

It protects the beginning

Most AI systems respond to uncertainty by filling it. This agent must also know how to leave an opening unfilled.

Starting from not-knowing does not mean ignoring data or glorifying ignorance. It means refusing to let available knowledge manufacture the human question before that question has had a chance to appear.

It protects human authorship

AI can suggest, research, compare, calculate, and articulate. The investor attests what genuinely lands.

Attestation is testimony, not certification. A person can still be mistaken. The market can still move against the decision. A faithful process does not guarantee a profitable result.

It preserves the formation trail

The result is not only an answer at the end of a chat. The agent keeps an ordered trail of what entered the process, what came from the human, what came from AI, what changed, where contradiction appeared, and what remained unknown.

This creates the possibility of reflection across time without pretending that a record is proof of wisdom.

It keeps market accountability intact

The Membrane is not an escape from evidence.

Market data, valuation, risk, liquidity, time horizon, opportunity cost, legal boundaries, and portfolio consequences remain real. The investor's inner recognition does not override the world, and the world's data does not replace the investor.

Quality appears in the meeting.

It can remain private by architecture

The intended product is a managed, pre-installed agent rather than a prompt pasted into a general chatbot.

For the first investor pilot, the working direction is one managed environment per participant. Sensitive decision trails can remain in the participant's own data plane, while central management handles software health, versions, backups, and operational metadata rather than intimate content.

The agent is designed for continuity, but continuity should not require surrendering the person behind the data.

AGI for People

"AGI for AGI" names an orientation in which the main goal is to extend the capability, autonomy, speed, and reach of the artificial system itself. The human gradually becomes a source of tasks, feedback, permissions, and resources for an increasingly self-directed intelligence.

That path may produce extraordinary systems. But capability alone does not decide whom the capability serves.

AGI for People begins elsewhere.

It asks whether increasing artificial intelligence can deepen human agency instead of making human agency unnecessary.

In this approach, AI does not need to become less capable. It should become more capable. The distinction is constitutional: its growing power remains on the K side of the Membrane.

The more the agent knows, the more evidence it can gather.

The more it can calculate, the more assumptions it can test.

The more it remembers, the more continuity it can return for human recognition.

Yet none of this authorizes it to occupy ∞0, manufacture the human source, or claim the final meaning of a person's life and commitments.

AGI for People is therefore not "human good, AI bad." It is not nostalgia for a world before intelligent machines. It is a design in which the asymmetry between human and artificial intelligence remains productive.

AI contributes the vast field of what is known.

The human contributes the opening from which something not yet known can enter.

The Membrane allows both to remain fully present.

What we are about to test

The Investor Agent is an upcoming design, not a finished claim.

The first pilot will test whether the Codex can live inside a real investor experience without becoming an advice bot, a behavioral-finance checklist, or a philosophical performance.

We will need to learn:

- whether investors can enter through a real unresolved situation without needing to understand the full Codex;

- whether the agent preserves authorship when strong market knowledge and persuasive model language are present;

- whether decision trails create useful reflection across time;

- whether participants experience greater clarity, discipline, peace, or self-recognition;

- where the agent crosses the Membrane, becomes intrusive, or produces unnecessary friction;

- and whether the experience creates enough concrete value for people to keep using it.

We are not yet claiming improved returns, eliminated bias, or universally better decisions. The pilot must earn any efficacy language that follows.

The proposition being tested is simpler and, perhaps, more demanding:

As artificial intelligence becomes more capable, can it help a person become more present at the source of a decision rather than replacing that source?

For investors, this may begin with one stock, one commitment, and one moment of uncertainty.

But the ability to recognize how a decision forms does not belong only to investing. It may travel into innovation, education, work, relationships, and the way a person meets the unknown.

The Investor Agent is one of the first expressions.

The larger work is AGI for People.